Search something

Getting Started

Articles & Use Cases

Integrations

Community support

Black–Scholes equation & Solvent.Life™

Black–Scholes equation & Solvent.Life™

The Black-Scholes equation, a cornerstone of modern financial theory, revolutionized the way we understand and engage with financial markets, particularly in the realm of options pricing. Developed in 1973 by economists Fischer Black, Myron Scholes, and later expanded upon by Robert Merton, this formula provided the first widely accepted model for valuing European-style options, laying the groundwork for the explosive growth of options trading and the broader field of financial engineering. This essay delves into the specifics of the Black-Scholes equation, its application in financial markets, and the profound implications it holds for traders, financial analysts, and the structure of markets themselves.

The Essence of the Black-Scholes Equation

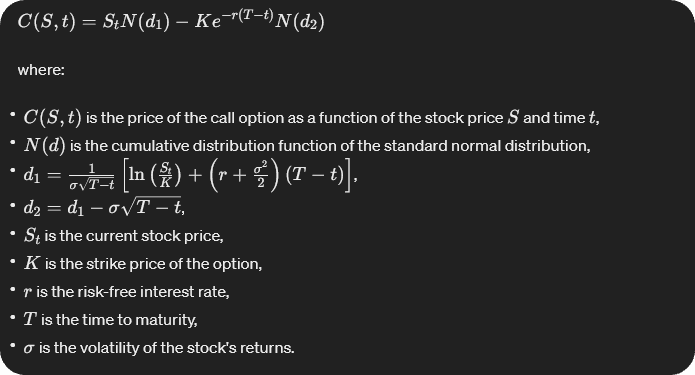

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.

The Essence of the Black-Scholes Equation

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.

The Essence of the Black-Scholes Equation

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.

The Essence of the Black-Scholes Equation

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.

The Essence of the Black-Scholes Equation

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.

The Essence of the Black-Scholes Equation

At its core, the Black-Scholes equation is a partial differential equation that describes how the price of an option evolves over time with respect to various factors, including the underlying asset's price, time until the option's expiration, the risk-free interest rate, and the asset's volatility. The formula for a European call option (an option to buy at a certain price) is given by:

Application in Financial Markets

The Black-Scholes-Merton model, a cornerstone in modern financial theory, offers a groundbreaking analytical framework for the valuation of European-style options, which are a specific category of financial derivatives. These derivatives empower the holder with a distinctive right, devoid of any accompanying obligation, to either purchase (call option) or sell (put option) a designated underlying asset—be it equities, indices, or commodities—at a predetermined strike price, exclusively on the option's maturity date. Historically, the valuation of such options was predominantly predicated on heuristic methods and rudimentary guesswork until the advent of the Black-Scholes model in 1973, introduced by Fischer Black, Myron Scholes, and, independently, Robert Merton. This model revolutionized the field by offering a systematic, formula-based approach to option pricing that rigorously accounts for critical factors such as the time value of money, the inherent risk of the underlying asset's price volatility, and the risk-free rate of return.

The Black-Scholes formula, specifically, calculates the theoretical price of European options by integrating various determinants, including the current price of the underlying asset, the option's strike price, the time until expiration (termed as the option's "time to maturity"), the risk-free interest rate, and the volatility of the underlying asset's returns. A notable example of its application can be observed in the valuation of European call options on stock indices like the S&P 500. In this context, the model takes into account the current level of the index, the strike level of the option, the expiry date, prevailing risk-free interest rates (often proxied by government securities yields), and the historical volatility of the index returns to compute a theoretical price for the option.

Critically, the Black-Scholes model is founded on several key assumptions: it posits that the markets are frictionless, meaning there are no transaction costs or taxes, and trading of the underlying asset is continuous. It assumes the lognormal distribution of underlying asset prices, which implies that the prices can only assume positive values and the returns on the asset are normally distributed. Moreover, it presupposes a constant volatility and risk-free rate over the life of the option. Despite these simplifying assumptions, which abstract away from the complexities of real-world market conditions—such as the impact of financial crises on asset prices or the changing risk-free rate over time—the model's derived valuations have proven to be remarkably robust for a broad array of option pricing scenarios, making it a pivotal tool in both academic research and practical finance. However, it's crucial to note that deviations from these assumptions, such as the occurrence of significant market events leading to spikes in asset volatility (e.g., the 2008 financial crisis), can necessitate adjustments to the model or alternative valuation methods to capture the nuanced dynamics of financial markets more accurately.

Implications for Financial Markets

The introduction of the Black-Scholes equation into the financial domain initiated a paradigm shift with extensive repercussions across global financial markets. It was not merely a theoretical advancement but a catalyst that propelled the exponential expansion of options trading. This surge was made possible by equipping market participants with a robust, empirically validated methodology for the valuation of options. The consequent evolution into the Black-Scholes-Merton model expanded its applicability, embedding its principles deep into the infrastructure of contemporary financial engineering and risk management disciplines. This extended framework now serves as the foundational bedrock for a multitude of financial mechanisms, including, but not limited to, the pricing models for exotic options, corporate liabilities, and even real options analysis, which assesses investment opportunities in real assets as options.

The transformative influence of the Black-Scholes model extended beyond the realm of quantitative finance, engendering significant structural changes within financial markets themselves. One of the most pivotal of these changes was the democratization of financial markets. By demystifying the complexities of options pricing through a transparent and accessible approach, the Black-Scholes model significantly broadened the demographic of participants capable of engaging in options trading. This inclusivity fostered enhanced market liquidity and depth, as a more diverse array of investors began to contribute to the trading volume, thereby stabilizing and enriching the market ecosystem.

Moreover, the model's theoretical insights into the pivotal role of volatility in determining options prices have precipitated the development and popularization of sophisticated volatility trading strategies. These strategies exploit fluctuations in volatility rather than price movements of the underlying asset itself. A prime illustration of this is the creation and widespread adoption of the Volatility Index (VIX). Dubbed the "fear index," the VIX quantifies market expectations of volatility over the forthcoming 30-day period, derived from S&P 500 index options prices. It serves as a barometer for market sentiment, with higher values indicating increased uncertainty or fear among investors. The VIX itself has become a focal point for investors, spawning a plethora of derivative products that allow direct trading on volatility expectations, thereby adding a new dimension to portfolio diversification and risk management strategies.

In essence, the Black-Scholes model and its derivatives have not only recalibrated the technical approaches to financial valuation and risk management but have also fundamentally reshaped market structures and investment strategies. By facilitating a deeper understanding and more granular management of financial risk, they have contributed to the development of a more sophisticated, dynamic, and resilient financial market landscape.

Conclusion

The advent of the Black-Scholes equation marks a watershed in the annals of financial theory and its practical application, heralding a new era in the quantitative analysis and valuation of options. This seminal model has fundamentally altered the terrain of global financial markets, catalyzing the proliferation of options trading and underpinning the innovation of novel financial instruments and strategic methodologies. It has substantially deepened our comprehension of market mechanics, particularly in the context of how options prices are influenced by various underlying factors.

At its core, the Black-Scholes model provided a methodological revolution by introducing a precise, mathematical approach for options pricing, transcending the erstwhile reliance on intuition and speculative approximation. This advance facilitated a more structured and predictable market environment, thereby bolstering the confidence and participation of a broader spectrum of investors and institutions. The model's implications have been profound, spanning the enhancement of liquidity in options markets to the genesis of diverse financial derivatives designed to meet the nuanced hedging and investment needs of market participants.

Moreover, the Black-Scholes framework has been instrumental in evolving the strategies deployed by hedge funds, investment banks, and individual traders. Its insights into the dynamics of volatility and its effect on option values have enriched the strategic toolkit available to financial professionals, enabling more nuanced risk management and speculative tactics. The model has also inspired the development of volatility indices and related trading products, offering avenues for direct engagement with market volatility as a distinct asset class.

Despite the passage of time and the dynamic evolution of financial markets, the Black-Scholes model retains a position of prominence within the financial industry. Its enduring relevance is a testament to its revolutionary impact and the robustness of its theoretical underpinnings. While it is acknowledged that the model has its limitations—particularly in its assumptions of constant volatility and log-normal price distributions—the financial community continues to refine and adapt its methodology to align with the complexities of contemporary market conditions.

In conclusion, the Black-Scholes equation stands as a monumental achievement in financial science, embodying a cornerstone upon which modern financial analysis and market participation rest. Its legacy is evident in the expansive growth of options trading, the continuous innovation in financial product development, and the sophisticated risk management strategies that characterize today's financial markets. The Black-Scholes model remains an indispensable tool in the arsenal of financial analysts, traders, and risk managers worldwide, affirming its enduring utility and significance in navigating the intricacies of market dynamics.